Refinancing: What Is It and How Can It Benefit You?

November 27, 2024 | Posted by: Sherry Corbitt

What is a refinance, and why should you care about it? Refinancing means renegotiating the terms of your mortgage, usually to access equity, and ideally should have lower borrowing costs (IE: lower interest rate). When you are a homeowner, as you pay your mortgage each month, complete improvements throughout your home, and as the real estate market changes, you build equity or value in your home. Meaning your house becomes worth MORE than what is left owing on your mortgage.

If you run into financial difficulty, want to complete much-needed home renovations, or are looking to purchase a second property, you can tap into that equity through various options. Most commonly, a borrower would choose to refinance because they could receive a better rate, change the amortization, switch the mortgage type, or access equity.

Interest rates have been steadily dropping, and many clients that received what a significant rate of 3 or 4% 3-5 years ago was, have now found that by refinancing and taking a lower rate (in the 1.95-2.5% range), they could save THOUSANDS of dollars in interest over the life of their mortgage! The benefit to working with a Mortgage Broker is that we proactively search for the best terms and rates for your SPECIFIC situation so you don’t have to spend hours calling from bank to bank to see what can be offered.

*NOTE* It is always best to find out your penalty to break your mortgage early if you want to refinance mid-term. A refinance does not make sense for every client.

Lengthening the amortization of your mortgage can mean lowering your monthly payments. This can equate to more interest paid in the long term. However, if your goal is to free up additional cash every month toward higher interest debts, this could make sense. This is especially true if your financial situation has taken a turn for the worse since taking out the mortgage. Just by changing the amortization of your mortgage, you could potentially free up enough cash to be able to stay in your home instead of selling. In combination with lengthening the amortization, borrowers often take out equity at the same time. This allows them to use the funds for home improvements, debt consolidation, or to take advantage of the rising real estate market to put some extra cash aside for emergencies. By taking out a larger mortgage, you are borrowing the funds at the lowest possible interest rate. If you are left with a better mortgage deal, in the end, all the better!

On the flip side, shortening the amortization increases your monthly payments but pays less interest overall. Additionally, you will become mortgage-free faster and ultimately end up with substantially more money in your pocket on a monthly basis.

As the economy and your finances change, it may make sense to change your mortgage type. When you purchased your home, you may have been more comfortable in the stability of having a fixed-rate mortgage. Your monthly payment would always remain the same during the length of your term, and no changes would be made. Now, switching to a variable rate mortgage could let you take advantage of today’s lowest interest rates and also ensures the lowest penalty in the event you need to break your term early.

Alternatively, you may have a variable rate mortgage and feel that now might be a good time to lock in and secure your rate for a long term due to the current economy and dropping interest rates. With so many options available as a homeowner, navigating what choice is best for your unique situation can be challenging. I am happy to review your circumstances and discuss how I can help improve your situation. Reach out today for your free mortgage review!

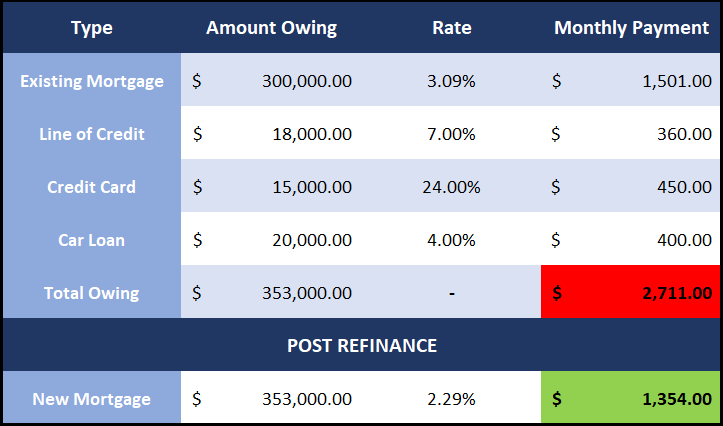

See an example refinance laid out below where the client would save $1357 per month by consolidating their debts into their mortgage!

Please reach out to me if you have any questions, I am always here to help with your mortgage needs!

Your Broker for Life,

Sherry Corbitt